Readers ask:

I’ve always heard about the strength and weakness of the US dollar. Can you provide basic background on what this means? What are the weaknesses for other currencies, especially all currencies in the basket? Is this a good or bad for my portfolio, which is mainly in US stocks and bonds? What are the main advantages and disadvantages of strong or weak dollars?

This is a timely question, as we have seen a big move in the dollar this year.

This is a fairly large move for the global reserve currencies, down around 7% per year.

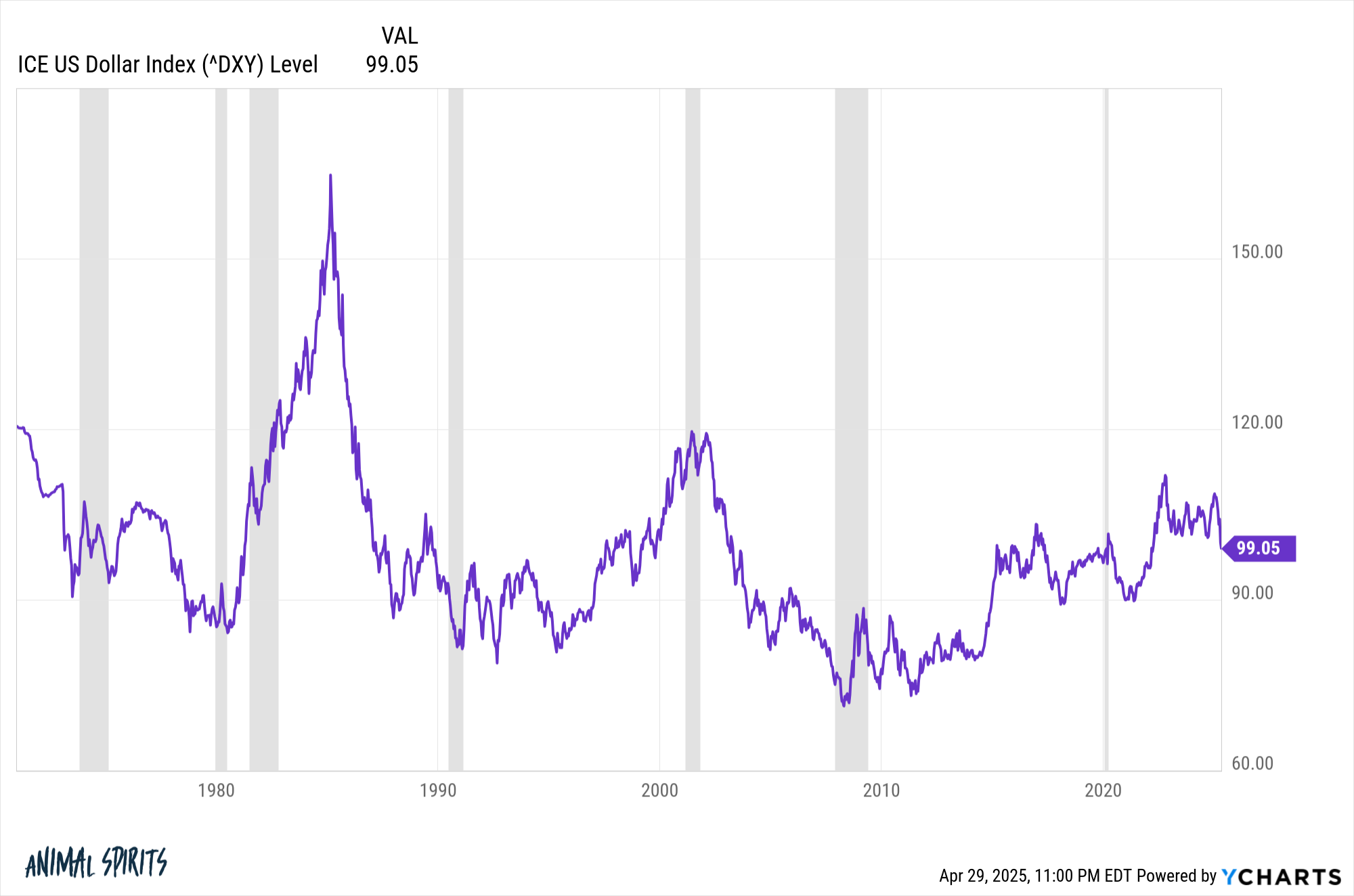

First, let’s take a look at the dollar’s movements over the long term.

This chart shows dollars dating back to the 1970s against baskets of foreign currency. There were many different regimes here – strong dollars, weak dollars, sideways dollars, etc.

But for over 50 years, the dollar has more or less gone anywhere. Like a character from a Rooney Tune, he spins his feet without going anywhere.

That strength or weakness can arise due to differences in interest rates, inflation, economic growth, or the flow of investments from foreign investors. There are many variables that affect your currency. Trust and faith in the system are unquantified.

A strong dollar tends to lower overseas sales, while a low dollar tends to increase overseas sales. If the dollar is weak, you can expect international stocks to surpass US stocks. That’s when foreign currency rates that investments in these countries will result in more profits in terms of revenue and dividends.

Once a dollar is strengthened, the opposite is true. Think about all those who go on vacation to Europe in recent years. The dollar was strong, but the euro was weak, making it cheaper for US tourists to travel abroad.

This is one of the reasons international stocks have long been performing poorly. Strong dollars are headwinds.

These currencies are another advantage of international diversification.

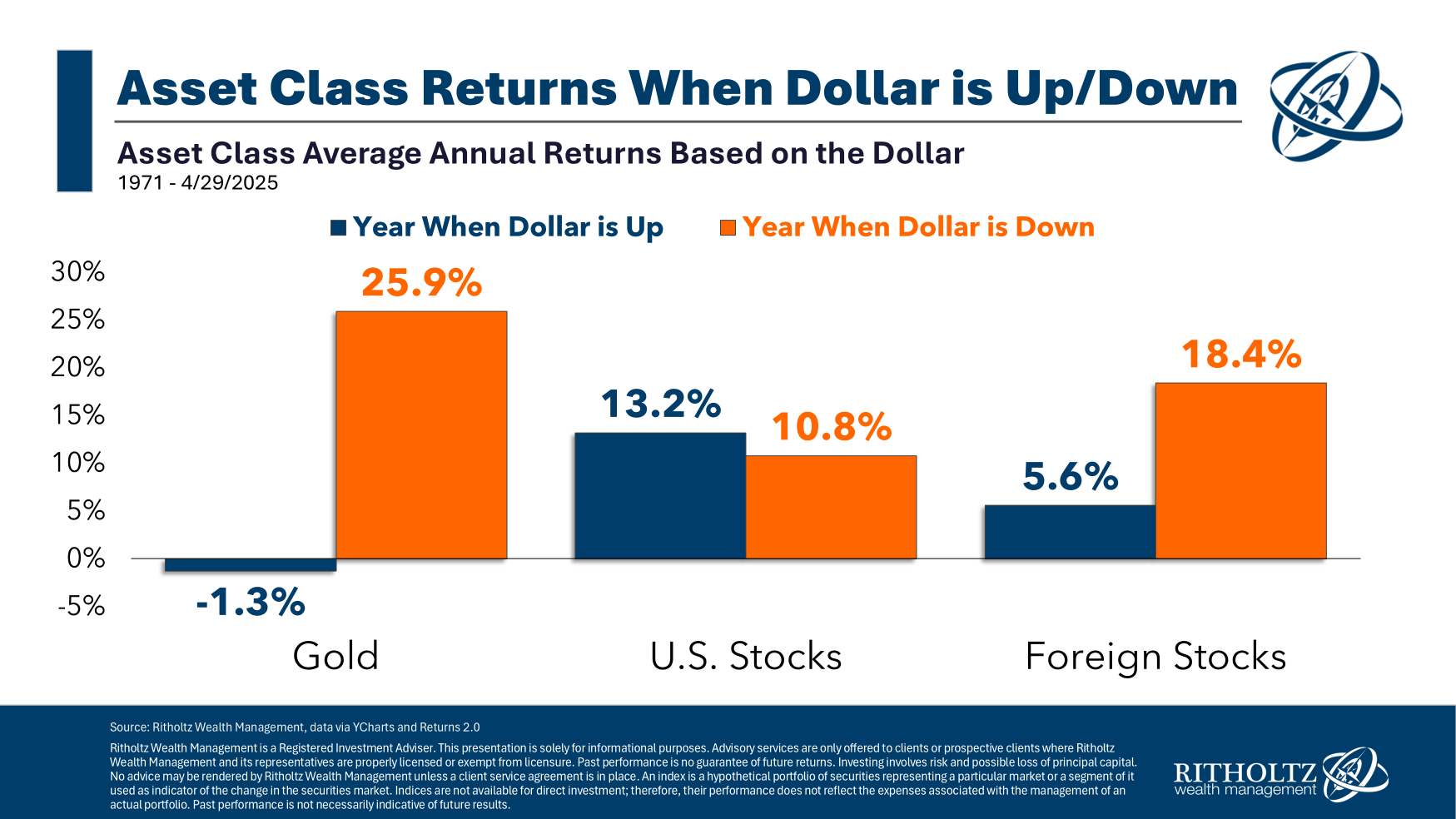

Let’s take a look at the historical number of stock market performance during a period of strong and weak dollars:

There is a clear pattern here.

With a strong dollar regime, US stock prices are outperformed, while in the weakness of the dollar regime, foreign stock prices are superior.

Market relations are not written on stone, so who knows whether this trend will continue, but it is always true that weaker dollars will be better for foreign investment, and strong dollars will make them worse (from a currency perspective).

For foreign audiences, that’s the opposite. Foreign investors who have invested in US stocks in recent years have received great returns as well as a great boost from the rising dollar. A weak dollar will make stocks less attractive to foreign investors.

So let’s look at the impact of the dollar on the short-term basis of US stocks, international stocks and gold.

This chart shows what happens in years when the dollar goes up and down from the next year.

The impact on US stocks is negligible, but look at how good gold and international stocks are when the dollar is weakening.

Again, we cannot promise that these relationships will be held, but this makes sense in theory as well. Gold prices are in dollars around the world. As the dollar weakens, it takes more time to buy the same ounce of gold. Internationally, however, more can now be purchased in yen, euros, or other currencies.

As far as bonds go, the standard answer is because that’s what you’re spending. Also, I don’t want to see bond yields hit by currency fluctuations.

This question has been further explained in more detail about Ask the Compound this week.

https://www.youtube.com/watch?v=ejjsvpeck_o

He also covered questions about crazy moves in the stock market, bond-to-high yield savings accounts, how to plan layoffs, and teaching high school students about personal finance.

Read more:

Is international diversification finally working?

This content, including security-related opinions and information, is provided for informational purposes only and should not be relied upon in any way as professional advice or endorsement of practices, products or services. There is no guarantee or guarantee that the views expressed herein may be applicable to any particular fact or situation. You should consult your own advisor regarding legal, business, tax, and other related matters related to your investment.

The commentary on this “post” (including related blogs, podcasts, videos and social media) reflects the personal opinions, perspectives and analysis of employees at Ritholtz Wealth Management who provide such comments and should not take into account the views of Ritholtz Wealth Management LLC. or as a description of the advisory services provided by the performance returns of their respective affiliates or Ritholtz Wealth Management or Ritholtz Wealth Management Investments clients.

Any reference to securities or digital assets, or performance data, is for example purposes only and does not constitute an investment recommendation or offer to provide investment advisory services. The charts and graphs provided internally are for informational purposes only and should not be relied upon when making investment decisions. Past performance does not indicate future results. Content will only be spoken as of the date indicated. The forecasts, estimates, forecasts, targets, outlooks and/or opinions expressed in these materials are subject to change without notice and may differ from opinions expressed by others.

Compound Media, Inc., an affiliate of Ritholtz Wealth Management. receives payments from various entities for related podcasts, blogs and email ads. The inclusion of such advertisements does not constitute or imply any endorsement, sponsorship or recommendations or affiliation by the Content Creator or Ritholtz Wealth Management or its employees. Investing in securities involves the risk of loss. For additional advertising disclaimers, please visit: https://www.ritholtzwealth.com/advertising-disclaimers

Please see disclosure here.